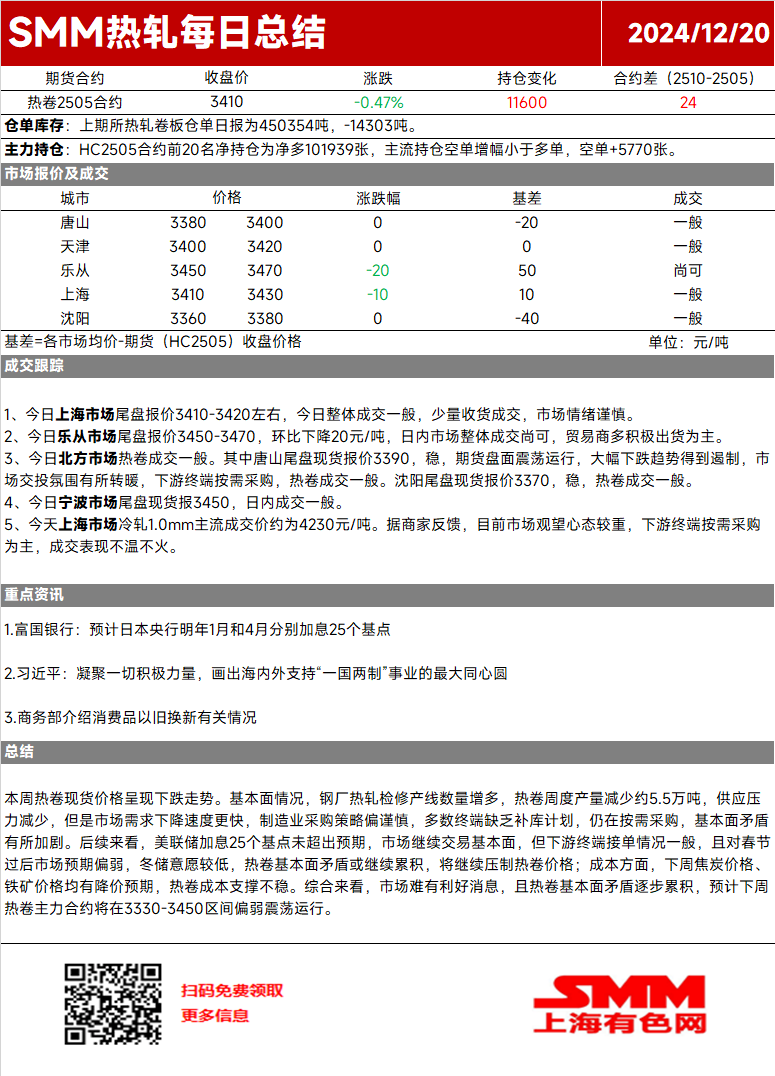

This week, HRC spot prices showed a downward trend. Fundamentals: The number of steel mill hot-rolling maintenance lines increased, reducing weekly HRC production by approximately 55,000 mt. While supply pressure eased, market demand declined at a faster pace. Manufacturing purchasing strategies remained cautious, with most end-users lacking restocking plans and continuing to purchase as needed, exacerbating fundamental imbalances. Looking ahead, the US Fed's 25-basis-point rate hike was within expectations, and the market continues to focus on fundamentals. However, downstream end-user order-taking remained moderate, and expectations for the post-Chinese New Year market were weak, with low winter stockpiling willingness. Fundamental imbalances in HRC may continue to accumulate, further weighing on HRC prices. Cost side, coke prices and ore prices are both expected to decline next week, weakening cost support for HRC. Overall, the market lacks positive news, and HRC fundamental imbalances are gradually accumulating. The most-traded HRC contract is expected to fluctuate downward within the 3,330-3,450 range next week.

[SMM HRC Daily Review] Unstable Cost Support; HRC Prices May Fluctuate Downward Next Week

【Unstable Cost Support, HRC Prices May Fluctuate Downward Next Week】This week, HRC spot prices showed a downward trend. Fundamentals: The number of steel mill hot-rolling maintenance production lines increased, reducing weekly HRC production by approximately 55,000 mt. While supply pressure eased, market demand declined at a faster pace. Manufacturing purchasing strategies remained cautious, with most end-users lacking restocking plans and continuing to purchase as needed, exacerbating fundamental imbalances. Looking ahead, the US Fed's 25-basis-point rate hike was in line with expectations, and the market continues to focus on fundamentals. However, downstream end-user order-taking remained moderate, and expectations for the post-Chinese New Year market were weak, with low winter stockpiling willingness. Fundamental imbalances in the HRC market may continue to accumulate, further weighing on HRC prices. On the cost side, coke prices and ore prices are expected to decline next week, leading to unstable cost support for HRC. Overall, with limited positive news and accumulating fundamental imbalances in the HRC market, the most-traded HRC contract is expected to fluctuate downward within the 3,330-3,450 range next week.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

Feb 6, 2026 18:30

Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].

Read More

Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].

This week, ferrous metals were in the doldrums, with coking coal and coke staging a mid-week rise. At the beginning of the week, financial markets experienced sharp fluctuations, dragging down sentiment in the ferrous chain and leading to a pullback in futures. Mid-week, Indonesia's cut to coke production quotas drove coking coal and coke futures to lead the gains, though the impact was more pronounced on thermal coal, while coking coal's rise was largely sentiment-driven and short-lived. In the latter part of the week, finished products continued their seasonal inventory buildup, and support from the raw material side weakened, causing the entire ferrous chain to pull back. In the spot market, with the Chinese New Year holiday approaching, purchasing activity slowed down further, with end-users only making limited, as-needed purchases at low prices.

Feb 6, 2026 18:30

Feb 6, 2026 18:09

MMi Daily Iron Ore Report (February 6)

Read More

MMi Daily Iron Ore Report (February 6)

Today, the DCE iron ore futures continued to hit bottom today, with the most-traded contract I2605 closing at 760.5 yuan/mt, down 1.23% from the previous trading day. Spot prices fell by 5–10 yuan/mt compared to the previous trading day.

Feb 6, 2026 18:09

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)

Feb 6, 2026 17:41

[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday

Read More

[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday

[SMM Chrome Daily Review: Trading and Inquiries Weakened, Chrome Market Showed Mediocre Performance Before the Holiday] February 6, 2026: Today, the ex-factory price of high-carbon ferrochrome in Inner Mongolia was 8,500-8,600 yuan/mt (50% metal content), flat MoM from the previous trading day...

Feb 6, 2026 17:41

Related News

Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].

Feb 06, 2026 18:30

MMi Daily Iron Ore Report (February 6)

Feb 06, 2026 18:09

[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday

Feb 06, 2026 17:41

[Daily Trading of SMM Hot-Rolled Coil] Futures fluctuated, spot trading further weakened.

Feb 06, 2026 17:37